AP Macroeconomics: Unit 4 - The Financial Sector & Money

Financial Assets

Financial assets are liquid claims on real assets or the income generated by them. In AP Macroeconomics, understanding the trade-off between risk, return, and liquidity is essential.

Key Concepts

- Liquidity: The ease with which an asset can be converted into cash (the medium of exchange) without significant loss of value.

- Example: Cash is perfectly liquid. Real estate is illiquid.

- Interest Rate: The price of borrowing money or the return on lending money.

- Opportunity Cost: The opportunity cost of holding money (cash) is the interest you could have earned if you had purchased an interest-bearing asset (like a bond) instead.

Stocks vs. Bonds

| Feature | Stocks (Equity) | Bonds (Debt) |

|---|---|---|

| Definition | Ownership share in a corporation. | A loan (IOU) represented by a certificate. |

| Status | Owner/Shareholder. | Lender/Creditor. |

| Return | Dividends & Capital Gains. | Interest payments (Coupon) & Face Value repayment. |

| Risk | Higher risk; last to be paid in bankruptcy. | Lower risk; paid before stockholders. |

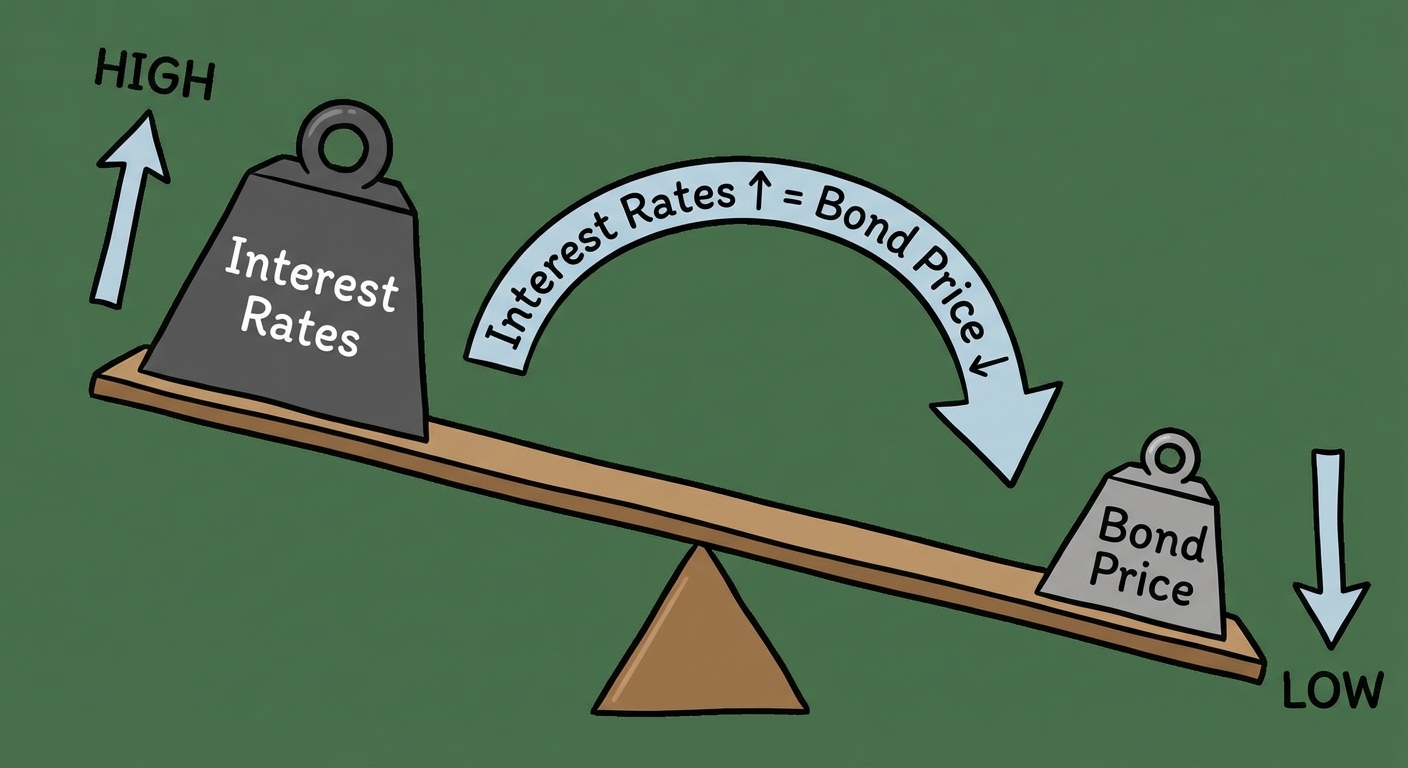

The Bond Market: Prices and Yields

This is one of the most frequently tested concepts in Unit 4. There is an inverse relationship between bond prices and interest rates.

The Logic:

- Imagine you buy a bond for $1,000 paying 5% interest ($50/year).

- Next week, the market interest rate rises to 10%.

- New bonds are now issued paying $100/year for the same $1,000 price.

- No one wants your "old" 5% bond unless you lower the price (sell it at a discount) to match the yield of the new bonds.

Rule of Thumb:

- Interest Rates $\uparrow$ $\rightarrow$ Bond Prices $\downarrow$

- Interest Rates $\downarrow$ $\rightarrow$ Bond Prices $\uparrow$

Definition, Measurement, and Functions of Money

Money is not just currency; it is any asset that can easily be used to purchase goods and services.

The Three Functions of Money

A handy mnemonic to remember these is M.U.S.:

- Medium of Exchange: Used to buy goods/services. It eliminates the "double coincidence of wants" required in a barter economy.

- Example: Buying a coffee with a debit card.

- Unit of Account: A measurement of value/price tag. It allows us to compare the worth of different goods.

- Example: Noting that a car costs $20,000$ and a bike costs $500$.

- Store of Value: It holds purchasing power over time (assuming inflation is not hyper-extreme).

- Example: Saving money in a jar to buy a phone next month.

Types of Money

- Commodity Money: Has intrinsic value (e.g., gold coins, cigarettes in prison, salt).

- Fiat Money: No intrinsic value; serves as money by government decree (e.g., paper US Dollars, Euro).

Measuring the Money Supply

The Federal Reserve categorizes money based on liquidity.

- M1 (High Liquidity):

- Currency in circulation (cash/coins).

- Checkable deposits (checking accounts).

- Traveler's checks.

- M2 (M1 + Near-Monies):

- Everything in M1.

- Savings accounts.

- Time deposits (CDs).

- Money market funds.

Note: Credit cards are NOT money contextually; they are a method of deferring payment (a liability/debt).

Banking and the Expansion of the Money Supply

Banks operate on a Fractional Reserve System, meaning they serve as financial intermediaries that hold only a fraction of their deposits as reserves and loan out the rest. This allows banks to "create" money.

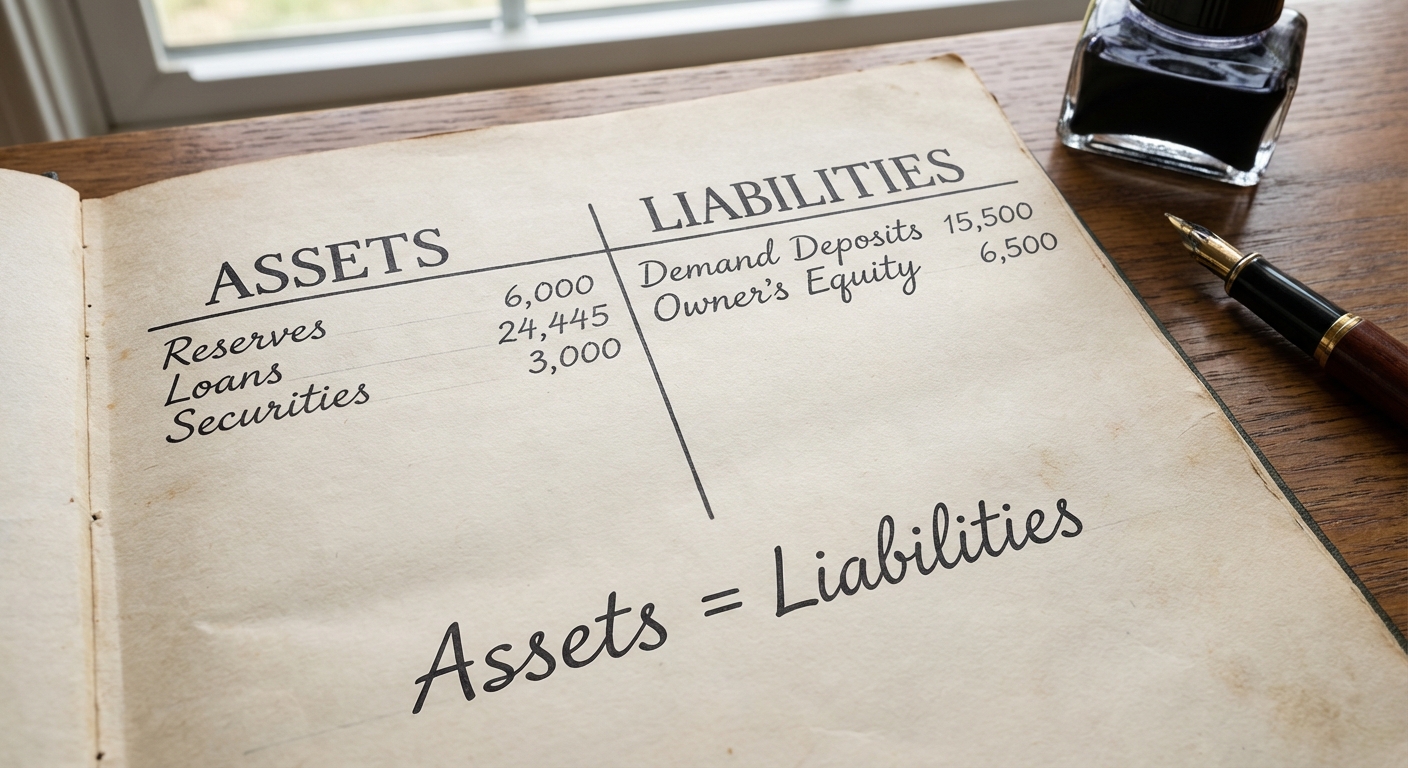

Bank Balance Sheets (T-Accounts)

A T-Account tracks a bank's Assets (what it owns or is owed) and Liabilities (what it owes to others). The sheet must always balance:

- Assets: Required Reserves, Excess Reserves, Loans, Bonds/Securities, Physical property.

- Liabilities: Demand Deposits (money owed to depositors), Owner's Equity.

Key Banking Definitions

- Required Reserves (RR): The specific % of demand deposits banks must keep in the vault or at the Fed.

- Excess Reserves (ER): Actual reserves minus Required reserves. This is the amount the bank can loan out.

The Money Multiplier

When a bank lends out its excess reserves, that money is deposited in another bank, which lends out a portion, and so on. This creates new money.

The Formula:

To calculate the Maximum Change in the Money Supply resulting from a generic injection of new reserves:

Worked Example:

Assume the Reserve Ratio is 10% ($0.10$). You deposit $1,000 cash (which was previously under your mattress) into Bank A.

- Liability increases: The bank owes you $1,000.

- Required Reserves: $1,000 \times 0.10 = \$100$.

- Excess Reserves: $1,000 - 100 = \$900$.

- Immediate M1 Change: $0$ (The cash was already M1; it just moved from your pocket to the bank).

- Potential New Money Created: The bank lends the $900.

The total money supply eventually increases by $9,000.

Common Pitfall: If the question asks for the total change in the money supply including the initial deposit (if the deposit came from the Fed, not your pocket), add the initial injection back in.

The Money Market

The Money Market graph illustrates the interaction between the demand for money and the supply of money, determining the Nominal Interest Rate.

1. Money Demand ($M_D$)

The demand curve is downward sloping due to the opportunity cost of holding money. As interest rates rise, people prefer to hold interest-bearing assets (bonds or savings) rather than cash.

Shifters of Money Demand:

- Price Level: If prices rise (inflation), you need more cash to buy the same goods. ($M_D$ shifts Right)

- Income (Real GDP): As income rises, people buy more things and need more liquid cash. ($M_D$ shifts Right)

- Technology: Credit cards and apps make it easier to pay without cash, decreasing demand for physical money. ($M_D$ shifts Left)

2. Money Supply ($M_S$)

The supply curve is Vertical. This is because the money supply is controlled by the Central Bank (The Federal Reserve) and is independent of the interest rate.

Shifters of Money Supply (Fed Monetary Policy):

- Reserve Requirement:

- Lower RR $\rightarrow$ More excess reserves $\rightarrow$ $M_S$ shifts Right.

- Discount Rate (Rate Fed charges banks):

- Lower rate $\rightarrow$ Easier to borrow $\rightarrow$ $M_S$ shifts Right.

- Open Market Operations (Buying/Selling Bonds): Most important tool.

- Buy Bonds: Fed gives banks cash for bonds $\rightarrow$ $M_S$ shifts Right (Big Money).

- Sell Bonds: Fed takes cash, gives rocks (bonds) $\rightarrow$ $M_S$ shifts Left (Small Money).

3. Equilibrium

The intersection determines the equilibrium Nominal Interest Rate ($i$).

- If the Fed increases Money Supply (shift Right), the Nominal Interest Rate falls.

- If the Price Level rises (Demand shifts Right), the Nominal Interest Rate rises.

Common Mistakes & Exam Pitfalls

- Bond Price vs. Interest Rate: Students often forget the inverse relationship. Repeat the mantra: "When rates go up, bond prices go down."

- Cash Deposits vs. Fed Purchases:

- If you deposit cash into a bank, the total Monetary Base doesn't change initially, only the composition (Currency $\rightarrow$ Demand Deposits).

- If the Fed buys bonds, it injects new money that wasn't there before. The total potential creation is usually higher.

- Calculation Limit: Remember that the "Total change in money supply" = Initial Injection $\times$ Multiplier. The "Loans Created" = Excess Reserves $\times$ Multiplier.

- Real vs. Nominal Rates: The Money Market graph always uses the Nominal Interest Rate on the Y-axis. The Loanable Funds Market (Unit 4, later section) uses the Real Interest Rate. Don't mix them up.

- Credit Cards: Remember, credit cards are not part of the money supply; they are a mechanism for deferring payment.