Unit 4: The Financial Sector – Mechanisms of Monetary Control

Introduction to Monetary Policy

Monetary Policy refers to the actions taken by a nation's central bank (such as the Federal Reserve in the U.S.) to manage the money supply and interest rates to achieve macroeconomic goals: stable prices, full employment, and sustainable economic growth.

While Fiscal Policy involves the government (taxes and spending), Monetary Policy involves the manipulation of the monetary base and checking deposits to influence the Aggregate Demand (AD) curve.

The Central Bank's Limited Reserves Framework

Historically, and for the purposes of the "Limited Reserves" model often tested on the AP exam, the central bank influences the economy using three primary tools. These manipulate the Money Market (Supply and Demand for Money).

Tools of Monetary Policy (Limited Reserves)

In a banking system with limited reserves, small changes in the supply of reserves affect the federal funds rate significantly. The Fed uses three levers:

1. Reserve Requirements (RR)

The Reserve Requirement is the fraction of total deposits that banks must hold in reserve and cannot loan out.

- Formula for Money Multiplier:

- Expansionary Action: Lowering the RR. This creates excess reserves, allowing banks to loan more money, increasing the Money Supply.

- Contractionary Action: Raising the RR. This forces banks to hold more cash, reducing lending ability.

2. The Discount Rate

The Discount Rate is the interest rate the Federal Reserve charges commercial banks for short-term loans.

- Expansionary Action: Lowering the discount rate makes it cheaper for banks to borrow reserves if they fall short. This encourages lending.

- Contractionary Action: Raising the discount rate discourages banks from borrowing reserves, tightening the money supply.

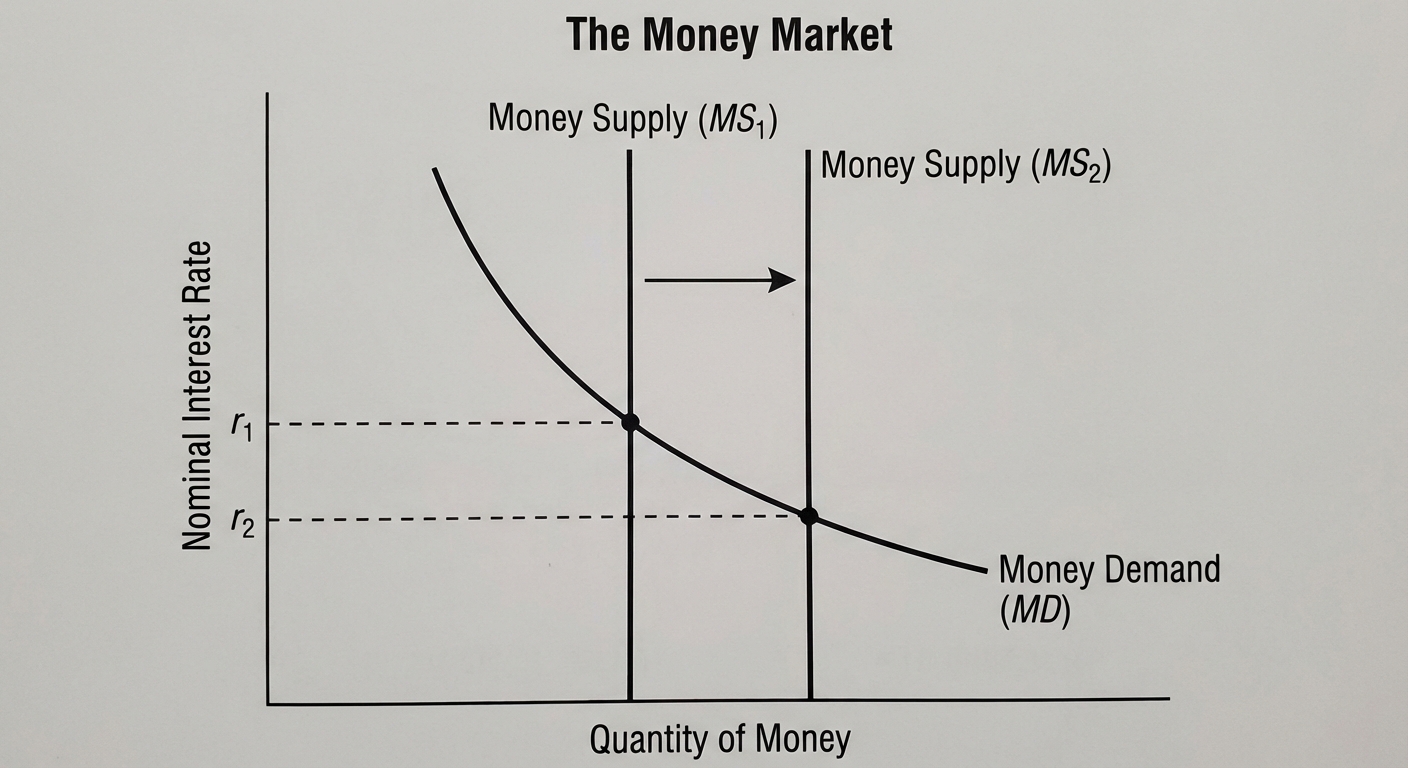

3. Open Market Operations (OMO)

This is the most frequently used tool in the traditional model. It involves the buying and selling of government securities (bonds) on the open market.

- Buying Bonds (Expansionary): The Fed buys bonds from banks and gives them cash (reserves) in return.

- Chain Reaction: Reserves $\uparrow$ $\rightarrow$ Money Supply $\uparrow$ $\rightarrow$ Nominal Interest Rates $\downarrow$ $\rightarrow$ Investment $\uparrow$ $\rightarrow$ AD $\uparrow$.

- Selling Bonds (Contractionary): The Fed sells bonds to banks and takes their cash.

- Chain Reaction: Reserves $\downarrow$ $\rightarrow$ Money Supply $\downarrow$ $\rightarrow$ Nominal Interest Rates $\uparrow$ $\rightarrow$ Investment $\downarrow$ $\rightarrow$ AD $\downarrow$.

Memory Aid: "Triple B"

Buy Bonds = Bigger Bucks (Money Supply Increases)

Sell Bonds = Small Bucks (Money Supply Decreases)

The Loanable Funds Market

While the Money Market determines nominal interest rates based on liquid cash preference, the Loanable Funds Market determines the Real Interest Rate ($r$). This market models the interaction between borrowers (demand) and savers (supply).

1. Supply of Loanable Funds

Who supplies the funds? Savers.

- Private Savings: Households saving money in banks.

- Public Savings: Government budget surplus (Tax Revenue > Gov Spending).

- Foreign Capital Inflows: Foreign investors putting money into domestic assets.

- Relationship: Direct relationship between real interest rate and quantity supplied (higher rates incentivize saving).

2. Demand for Loanable Funds

Who demands the funds? Borrowers.

- Investment: Firms borrowing to buy capital goods.

- Government: Borrowing to fund budget deficits.

- Relationship: Inverse relationship between real interest rate and quantity demanded (higher rates make projects less profitable).

3. Key Shifters

| Curve | Shifter Example | Effect |

|---|---|---|

| Demand $\uparrow$ | Gov. Deficit Spending | Real Interest Rate $\uparrow$ (Crowding Out) |

| Demand $\uparrow$ | Business Confidence | Real Interest Rate $\uparrow$, Quantity Loans $\uparrow$ |

| Supply $\uparrow$ | Increased Savings Rate | Real Interest Rate $\downarrow$, Quantity Loans $\uparrow$ |

| Supply $\downarrow$ | Capital Flight (Outflow) | Real Interest Rate $\uparrow$, Quantity Loans $\downarrow$ |

Crowding Out Effect

When the government runs a deficit, it must borrow from the Loanable Funds Market. This shifts the Demand for Loanable Funds to the right.

Result: The Real Interest Rate increases. Because borrowing is now more expensive, private investment decreases. The government spending "crowds out" private investment.

The Quantity Theory of Money

This theory relates the money supply to inflation and overall economic output. It is theoretically grounded in the Equation of Exchange:

Variables Defined

- $M$: Money Supply (M1 or M2)

- $V$: Velocity of Money (How many times the average dollar is spent per year)

- $P$: Price Level (Aggregate price of goods)

- $Y$: Real GDP (Output)

- Note: $P \cdot Y$ equals Nominal GDP.

The Monetarist View

Monetarists assume that the velocity of money ($V$) is relatively constant/stable and that Real Output ($Y$) is determined by resources and technology (independent of money in the long run).

Therefore, if $V$ and $Y$ are constant, any increase in the Money Supply ($M$) creates a proportional increase in the Price Level ($P$).

Example: If the Central Bank doubles the money supply, and velocity/output are constant, the price level will double (100% inflation).

Common Mistakes & Pitfalls

Money Market vs. Loanable Funds

- Mistake: Mixing up the interest rates.

- Correction: The Money Market (Liquidity Preference) determines the Nominal Interest Rate. The Loanable Funds Market determines the Real Interest Rate.

Bond Prices vs. Interest Rates

- Mistake: Thinking bond prices and interest rates move together.

- Correction: They have an inverse relationship. When the Fed sells bonds (increasing supply of bonds on the market), bond prices drop, and the effective interest yield rises.

Real vs. Nominal Interest Rate Formula

- Mistake: Forgetting how inflation bridges the two.

- Correction: Remember the Fisher Equation:

"Crowding Out" Logic

- Mistake: Thinking Crowding Out decreases interest rates.

- Correction: Government borrowing increases the Demand for loans, which increases interest rates, which subsequently makes it too expensive for businesses to borrow.