Unit 1: Decision Making and Economic Structures

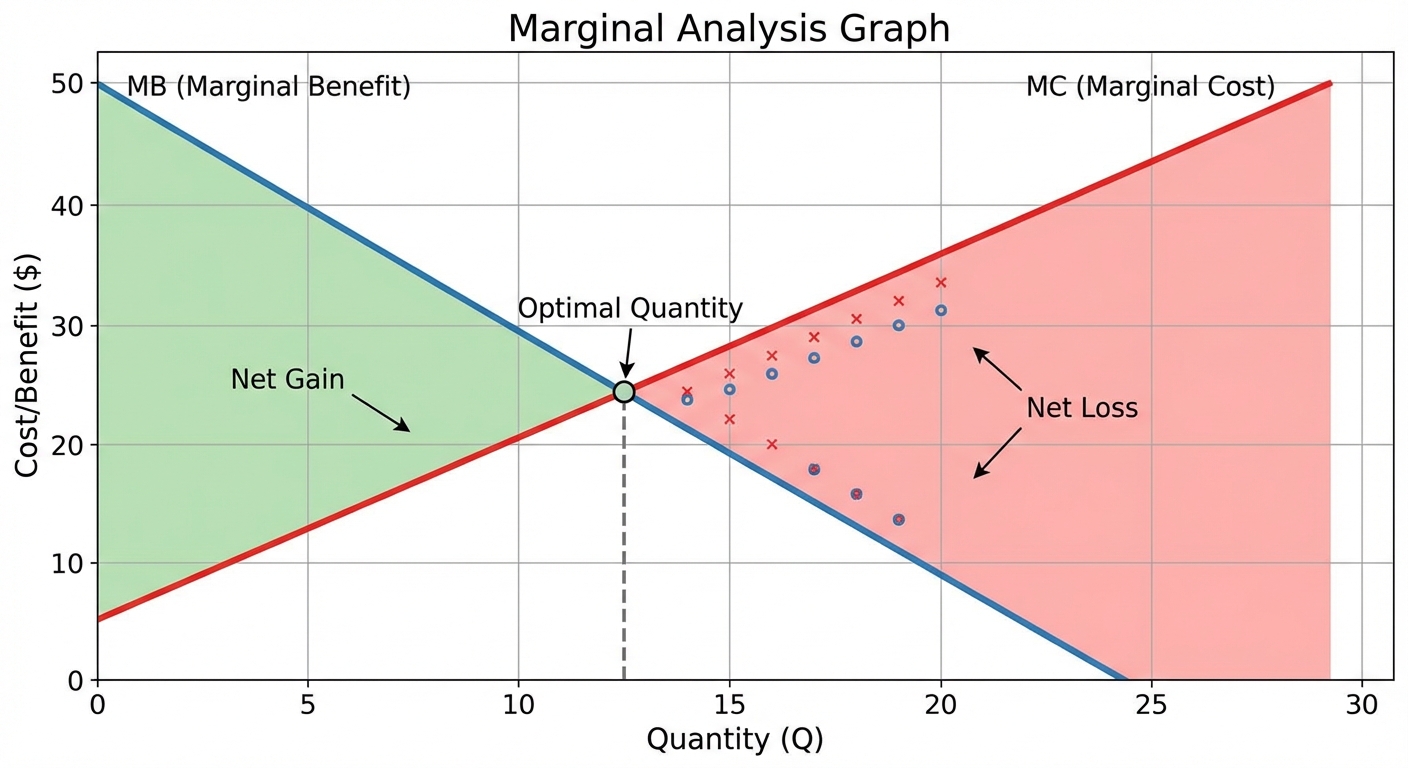

Marginal Analysis

Economics is effectively the study of choices. While scarcity forces us to make choices, Marginal Analysis (also known as "thinking at the margin") is the mathematical and conceptual tool used to verify if those choices are rational.

The Core Concept

Most decisions in life are not "all or nothing." You do not decide between studying for 24 hours or 0 hours; you decide whether to study for one more hour.

- Marginal Benefit (MB): The additional satisfaction or utility derived from consuming or producing one more unit of a good or service.

- Marginal Cost (MC): The additional cost incurred from consuming or producing one more unit.

The Golden Rule of Maximization

Rational agents (consumers and producers) continue an activity as long as the marginal benefit exceeds the marginal cost. The optimal quantity is reached when:

- If $MB > MC$: You should do more of the activity (you gain net benefit).

- If $MB < MC$: You should do less of the activity (the cost outweighs the gain).

- If $MB = MC$: You are at the optimal level. Total Net Benefit is maximized.

Example: The Pizza Scenario

Imagine you are hungry and buying slices of pizza.

| Slice # | Marginal Benefit (Utility) | Marginal Cost (Price) | Decision |

|---|---|---|---|

| 1 | $10 | $3 | Buy (Net gain +$7) |

| 2 | $8 | $3 | Buy (Net gain +$5) |

| 3 | $3 | $3 | Stop here (Optimal) |

| 4 | $1 | $3 | Don't Buy (Net loss -$2) |

Notice the Law of Diminishing Marginal Utility: As you consume more of a good, the satisfaction from each additional unit generally decreases (the first slice tastes better than the fourth).

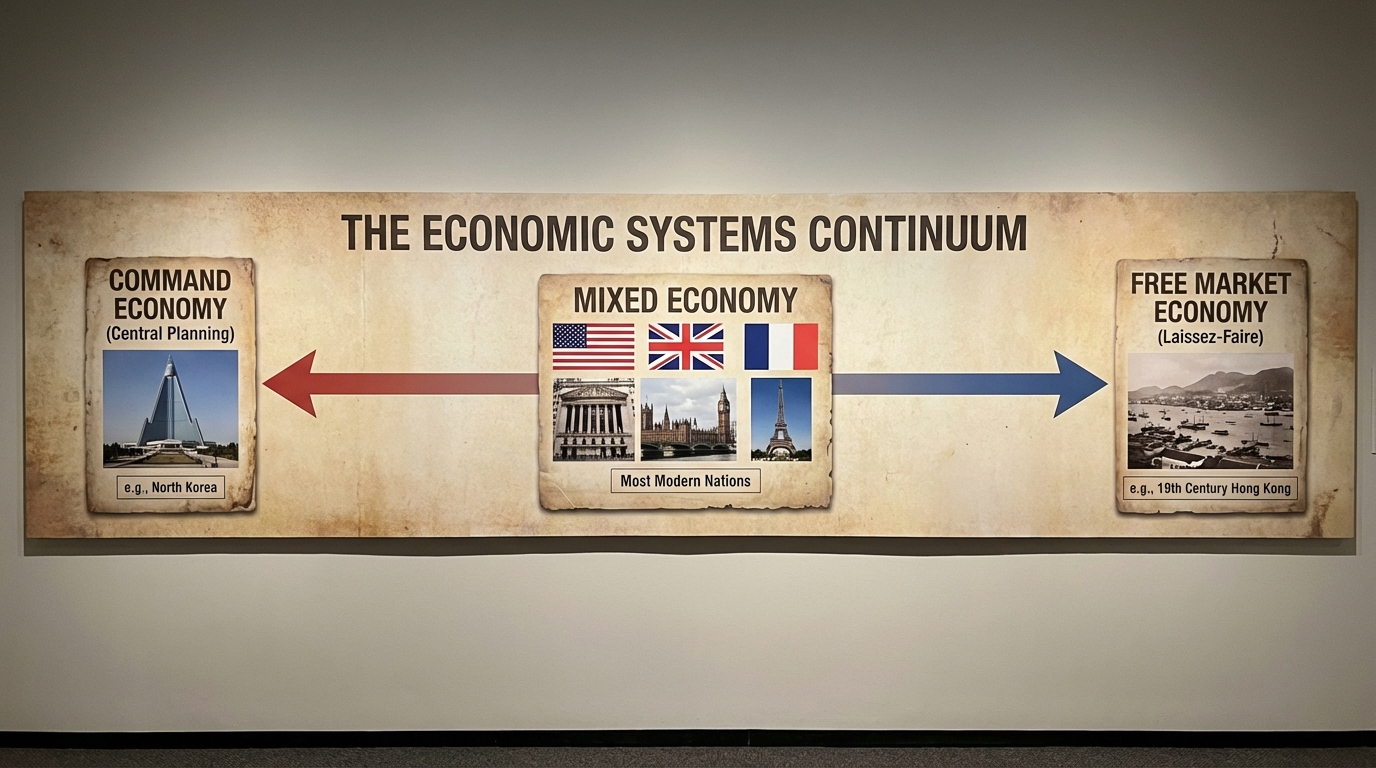

Economic Systems

Every society faces the problem of scarcity—limited resources but unlimited wants. To solve this, every society must answer three basic economic questions:

- What goods and services should be produced?

- How should these goods and services be produced?

- For Whom should these goods and services be produced?

An Economic System is the method a society uses to answer these questions. While there is a spectrum, we primarily analyze two opposing models and the middle ground.

1. The Command Economy (Centrally Planned)

In a command economy, the government or a central planning authority owns the resources and makes all economic decisions.

- Focus: Equity and stability (in theory).

- Mechanism: The government dictates quotas, prices, and wages.

- Weakness: Lack of incentives for innovation; difficult to calculate consumer wants efficiently (shortages/surpluses are common).

- Examples: North Korea, Former Soviet Union.

2. The Market Economy (Laissez-Faire)

In a pure market economy, individuals and private firms own resources. Decisions are made through voluntary exchange in markets.

- Focus: Efficiency and freedom.

- Mechanism: Price signals. Prices act as a communication tool between buyers and sellers.

- The Invisible Hand: A concept by Adam Smith suggesting that self-interested behavior in free markets leads to the most efficient social outcome.

- Weakness: Can lead to market failures (monopolies, externalities, inequality).

3. Mixed Economy

In reality, almost all modern economies are mixed economies. They utilize market mechanisms for most goods but include government intervention to protect property rights, provide public goods, and regulate markets.

Comparison Table

| Feature | Command Economy | Market Economy |

|---|---|---|

| Resource Ownership | Government (Public) | Individuals (Private) |

| Regulation | High | Minimal / None |

| Response to Scarcity | Central Planner allocates | Prices allocate via Supply & Demand |

| Incentive | Meeting Quotas / Patriotism | Profit / Self-Interest |

Property Rights and the Role of Incentives

For a market economy to function efficiently, the government must uphold the rule of law, specifically regarding property rights.

What are Property Rights?

Property Rights establish ownership and grant individuals the exclusive authority to determine how a resource is used. This includes:

- The right to use the good.

- The right to earn income from the good.

- The right to transfer (sell) the good to others.

If property rights are weak or non-existent (e.g., if the government can seize your factory at any time, or people can steal your invention without penalty), the market fails.

How Rights Create Incentives

Property rights are the fuel for the engine of the economy. They create incentives—motivating factors that influence behavior.

- Incentive to Produce & Invest: Only if you are guaranteed the right to keep the profit from your labor or investment will you take the risk to start a business.

- Incentive to Maintain: Owners take better care of resources than non-owners. (Think: Do people wash a rental car as carefully as their own car? No.)

- Incentive to Innovate: Intellectual property rights (patents, copyrights) encourage new technologies by granting temporary monopolies to inventors.

Summary of the Flow

Common Mistakes & Pitfalls

- Confusing Total vs. Marginal: A common exam trap shows Total Benefit increasing, but Marginal Benefit negative. Remember: if doing "one more" yields negative utility, don't do it, even if your total happiness is still high.

- The "Pure" Market Myth: Students often write that the US is a pure market economy. It is not; it is a mixed economy. Pure laissez-faire does not exist in the modern world.

- Ignoring the Role of Government in Markets: Students often think markets and government remain separate. However, markets require government to enforce contracts and property rights. Without government courts/police, a market devolves into theft.

- Optimal isn't Maximum Output: In marginal analysis, stopping where $MB=MC$ often means stopping before maximum capacity. You stop where profit is maximized, not necessarily where output is highest.